How I’m Turning $5,000 of Dead Money Into Tax-Free Growth?

I owe the IRS $10,000 every April. I don’t pay it through my paystub – I pay it all at once at tax deadline.

Why? Huge credit card signup bonuses. I’m always looking for ways to squeeze more out of a dollar.

I found a card with 0% APR for 12 months with a signup bonus. That’s when it hit me – why park the float in a savings account? Put it in the market instead. A Roth IRA. Tax-free growth instead of taxable interest.

Here’s what I did with $5,000 of that tax money, how it works, and what I’m tracking.

What is Stoozing

Stoozing is a UK term for borrowing at 0% and parking the money somewhere that earns interest, pocketing the spread. Traditionally people would take 0% balance transfer offers and stick the cash in a savings account.

I’m running a version of this – instead of a savings account, I’m using a Roth IRA invested in the market. Higher expected returns, higher risk.

More on traditional stoozing here.

My Situation

Between my job and side hustle, I owe around $10,000 in taxes every April.

Most people withhold through their paystub or pay quarterly. I don’t. I keep the full amount until tax deadline and pay it in one lump sum on April 15.

I do this for for credit card signup bonuses usually. This year I needed more time to let the money work, and that’s when the stoozing idea came up. The 0% APR made it possible.

I still meet the IRS safe harbor rule through W2 withholding. I pay at least 100% of last year’s tax liability through my regular job. No underpayment penalty, even though I’m not paying quarterly on the side hustle income.

The $10,000 I owe is the gap between what got withheld and what I actually owe.

For years that $10,000 just sat in checking waiting for the IRS. This year I started looking for something better than a high-yield savings account. That’s when the Roth IRA idea hit.

The $11.67 Problem

$5,000 in a high-yield savings account earns:

- 4% APY (Current rate) = $200/year gross

- Minus taxes (federal + state, roughly 30%) = $140/year net

- $140 ÷ 12 = $11.67/month

That’s the baseline.

Here’s how the options compare:

| Option | Annual Return | Monthly | Year-End Total |

|---|---|---|---|

| Checking | $0 | $0 | $5,000 |

| HYSA at 4% | $140 (after tax) | $11.67 | $5,140 |

| Roth IRA + SPY | $525 expected (tax-free) | $43.75 | $5,525 expected |

The HYSA number is the baseline I’m using – 4% is what’s available right now, but rates can drop if the Fed cuts. The SPY number is expected value based on historical averages – not guaranteed. SPY’s 1-year returns have a standard deviation around 15%, which means in any given year it could be down 20% or up 30%. The $525 is what the math says to expect over time, not what I’m guaranteed to get this year.

Difference between doing nothing and the Roth: $525 expected if SPY performs at its historical average. Difference between HYSA and Roth: $385 expected.

That $525 gain is tax-free if it happens. The HYSA interest gets taxed every year.

You can stack more by signing up for a Roth IRA through cashback portals like Swagbucks or Rakuten – earn an extra $20-40. I’m not doing that here, but it’s there if you want even more mula.

What This Experiment Is

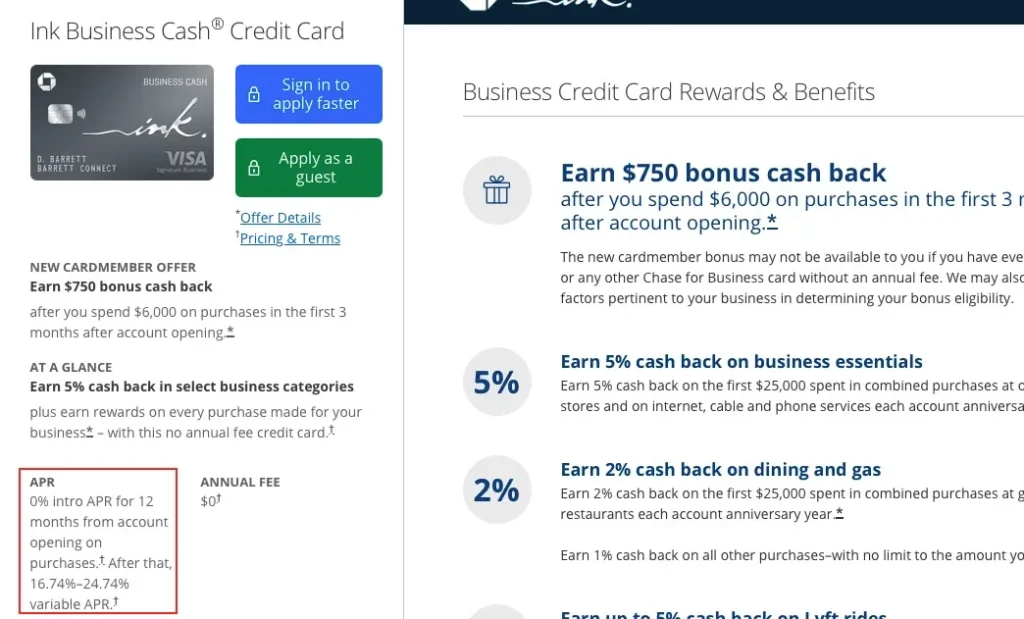

I’m using a Chase Ink Business card with 0% APR for 12 months. Please note this offer changes from time to time.

The mechanic: I charge normal business expenses to the card. The $5,000 cash that would have paid those expenses goes into a Roth IRA instead. I invest it in SPY. At month 11 – not 12, I’m giving myself a buffer – I pay the Chase balance in full.

The Roth stays invested. Whatever it’s worth at month 11 is mine. Tax-free.

The credit card isn’t producing returns. It’s operational – I could invest the $5,000 and pay expenses normally and get the same result. The card setup just makes it cleaner for me to mentally separate “tax money” from “invested money.”

This isn’t new money. I’m using $5,000 of my 2026 Roth IRA contribution limit ($7,500 total if you’re under 50). The other $2,500 I’m funding from regular cash flow.

The 0% APR window matters. After 12 months, Chase Ink APR jumps to 16.74%-24.74%. If I miss that deadline and carry a balance, I’m paying $837+ in interest on $5,000. That wipes out six years of HYSA profit.

Month 11 payoff is non-negotiable.

Why SPY – The 60-Year Case

I’m not picking a stock. I’m not betting on a sector. I’m betting the US economy doesn’t collapse in 12 months.

SPY tracks the S&P 500 – 500 of the largest US companies, weighted by market cap. Boring. Documented.

60 years of annual return data (1965-2024):

- Negative years: roughly 16 out of 60 (~27%)

- Positive years: roughly 44 out of 60 (~73%)

- Average positive year: +21%

- Average negative year: -14%

- Consecutive negative years: twice (1973/74, 2000/2002)

- Any 20-year period: never negative

- Any 30-year period: never negative

- Long-run average: 10-10.5% annualized with dividends

Worst single year was 2008: -38.5%. On $5,000, that’s a $1,925 paper loss. The Roth doesn’t close. The money doesn’t disappear. It stays invested and recovers.

What If COVID Happens Again

The 2020 pandemic crash is the most recent fast, brutal drawdown.

- February to March 2020: SPY dropped 34% in one month

- March to August 2020: fully recovered

- End of 2020: SPY was up 16% for the year

If a COVID-level event happens during my 12-month window and I hit month 11 at the bottom, I pay the Chase card with other cash. I don’t sell SPY at a loss. The Roth stays invested. The loss is on paper, not realized. The market recovers.

This only works if I have liquidity to cover the $5,000 card balance regardless of what SPY does. I do. That’s a prerequisite.

If you don’t have that cushion, don’t do this.

The Math Going In

$5,000 in SPY at 10.5% historical average for 12 months:

- Expected gain: $525 (tax-free)

- Monthly equivalent: $43.75

- vs. HYSA baseline: $11.67/month

Difference: +$32/month in expected value.

The real power is what happens if I leave it in the Roth:

| Years | Nominal Value at 10%/yr | Real Value (inflation-adjusted)* |

|---|---|---|

| 10 | $13,000 | ~$10,000 |

| 20 | $34,000 | ~$21,000 |

| 30 | $87,000 | ~$40,000 |

| 60 | $1,800,000 | ~$300,000-$400,000 |

*Assumes ~3% average inflation. Real purchasing power in today’s dollars.

All tax-free. No capital gains tax. No dividend tax. No withdrawal tax in retirement.

HYSA over 20 years at 2.8% net (after ongoing tax drag): $8,556 nominal, roughly $5,200 real.

Gap on this single $5,000 contribution after 20 years: roughly $15,000 in real purchasing power.

That’s the difference between taxable interest and tax-free compounding.

The Honest Risks

SPY could be down 20% at month 11 when I need to pay Chase. If that happens, I pay the card from other cash and leave SPY in the Roth to recover. I don’t sell at a loss.

This only works if I have liquidity separate from the Roth. I do. If you don’t, this doesn’t work.

If I miss month 11 and carry a balance past month 12, Chase starts charging 16.74% APR. On $5,000, that’s $837/year in interest. That wipes out the HYSA baseline for six years.

I have a calendar alert set. Non-negotiable.

Once the $5,000 goes into the Roth, it counts against my 2026 contribution limit ($7,500 total). I can withdraw contributions penalty-free anytime, but I lose that contribution room forever. Can’t “undo” it and get the space back.

This isn’t a liquid emergency fund strategy. One-way move.

This strategy works for people who are disciplined about payment deadlines and don’t panic sell when the market drops. If you forget deadlines, carry balances, or sell when things go red, don’t try this.

Why I’m Starting at $5,000 and Not $10,000

My total tax buffer is $10,000. I’m only using $5,000 for this.

Why not go all in?

Discipline. I want to see how this feels before I scale. If month 6 and month 9 updates show the plan is working and I’m not losing sleep, I’ll consider increasing to $10,000 next year.

Worst possible outcome is scaling up right before a bad year.

What I’m Tracking

Updates every 3 months:

- Q1 (Month 3): SPY price, portfolio value, vs. HYSA baseline ($35)

- Q2 (Month 6): Halfway check, running total vs. baseline ($70)

- Q3 (Month 9): Final stretch, card payoff confirmed

- Month 12: Card paid, final portfolio value, total gain/loss vs. $140 HYSA baseline

I’ll report the numbers whether they’re good or bad. A blog that only posts wins is marketing.

Disclaimer

Not a financial advisor. This is documentation, not advice. The numbers has been checked with Claude and ChatGPT but still verify your own numbers.

This requires liquidity to cover the credit card balance independent of market performance. If you don’t have that cushion, don’t try this.

Roth IRA contribution limits apply – this uses existing contribution room for 2026. Tax situations vary by state, income, and filing status. Consult a CPA.

Past S&P 500 performance doesn’t guarantee future results. The expected returns in this post are based on historical averages, not predictions.